2026 Housing Outlook: Insurers Cautiously Re-Enter California and Florida Markets Using Satellite Risk Modeling

The residential insurance markets in California and Florida have long been battlegrounds, plagued by escalating natural disaster risks and an often-combative regulatory environment. For years, major insurers have either pulled back entirely or significantly restricted new policies, leaving homeowners in these high-risk states struggling to find affordable coverage. However, as 2026 unfolds, a cautious optimism is emerging. Thanks to breakthroughs in satellite risk modeling and advanced geospatial analytics, some insurers are beginning to re-evaluate their strategies, leading to a measured re-entry into these challenging, yet lucrative, markets.

1. The Exodus: A Brief History of Retreat

California and Florida, with their vibrant economies and desirable climates, are also ground zero for some of the nation’s most devastating natural perils. California grapples with an increasing frequency and severity of wildfires, exacerbated by drought and urban sprawl into wildland-urban interface (WUI) zones. Florida, conversely, faces the relentless threat of hurricanes, storm surge, and rising sea levels, posing an existential risk to coastal properties.

These environmental challenges, compounded by what many insurers describe as burdensome regulatory frameworks and rampant litigation (particularly in Florida), led to an untenable situation. Between 2022 and 2025, major carriers like State Farm, Allstate, Farmers, and AAA either announced moratoriums on new policies, non-renewed existing customers, or significantly hiked premiums, making insurance virtually inaccessible for many. The result was a dramatic increase in reliance on state-backed “insurers of last resort”—California’s FAIR Plan and Florida’s Citizens Property Insurance Corporation—which were never designed to be the primary market.

The withdrawal wasn’t arbitrary. Insurers, fundamentally risk assessors, found their traditional actuarial models inadequate to price the rapidly evolving and intensifying risks. They lacked the granular data and predictive power to confidently underwrite policies without facing catastrophic losses. The sheer unpredictability of wildfire patterns or hurricane intensity, combined with the escalating costs of rebuilding, rendered profitability elusive.

2. The Tech Revolution: Satellite Risk Modeling to the Rescue

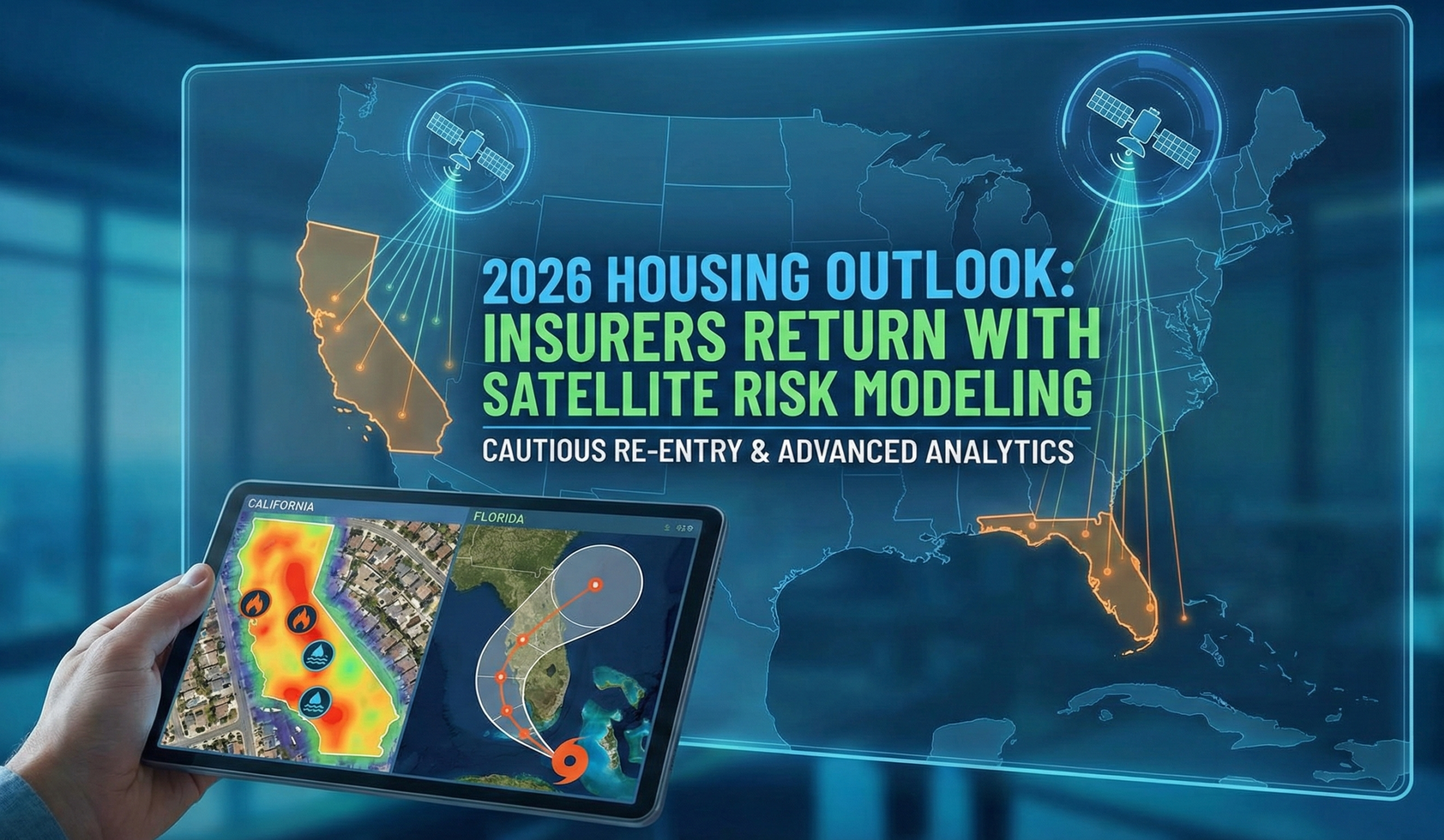

The turning point, according to industry analysts and emerging reports, lies in the maturation of satellite risk modeling. This isn’t just about looking at a property from above; it’s a sophisticated integration of multiple data streams, processed by AI and machine learning algorithms, to create hyper-localized, real-time risk assessments.

How it Works: Layers of Insight

- High-Resolution Imagery: Satellites now provide imagery at an unprecedented resolution, allowing insurers to identify specific structural features, roof conditions, surrounding vegetation (fuel load for fires), and proximity to water bodies or flood zones. This goes far beyond general zip code or county-level assessments.

- LIDAR (Light Detection and Ranging) Data: This technology provides precise topographical data, essential for modeling flood pathways, elevation changes, and the impact of storm surge on specific parcels. It can even map the height and density of vegetation around a home, a critical factor for wildfire risk.

- Historical and Predictive Weather Patterns: Integrating decades of historical weather data with advanced climate models, insurers can better forecast micro-climates, wind patterns, and the likelihood of extreme precipitation events at a very localized level.

- Vegetation Index and Fuel Load Mapping: For wildfire-prone areas, satellites can track the health and density of vegetation, identifying areas with high “fuel load” that are more susceptible to rapid fire spread. They can also monitor post-fire regrowth, informing recovery and mitigation efforts.

- Perimeter and Firebreak Analysis: In California, insurers are using satellite data to assess defensible space around properties, verifying if homeowners have cleared vegetation adequately—a critical factor in wildfire survival.

- Real-Time Monitoring: Some systems can even monitor active events. During a wildfire, satellites can track its perimeter, allowing insurers to anticipate potential claims and understand the trajectory of damage, even before on-the-ground assessments are possible. During a hurricane, they can map inundation zones post-storm.

This multi-layered approach allows insurers to move from generalized risk pools to individualized risk profiles. Instead of painting an entire zip code with a broad brush, they can now differentiate between two houses on the same street, offering coverage and pricing based on specific mitigation efforts, landscaping choices, and structural vulnerabilities.

3. Deep Dive: The End of “Collective Punishment”

During the crisis of 2022-2025, insurers abandoned entire zip codes. If you lived in a fire zone, it didn’t matter if your house was a concrete bunker; you got canceled just the same. The Revolution of 2026: Satellite modeling allows for Precision Underwriting.

- The Careless Neighbor: The satellite detects dry brush stacked against your neighbor’s wall. He pays more or loses his policy.

- The Responsible Owner: The same satellite sees that you have created a 30-foot “defensible space” and installed a new roof. You get coverage.

- Why it matters: This rewards individual effort over general statistics.

4. The Cautious Re-Entry: A Strategy of Precision

While satellite modeling offers powerful new tools, the re-entry into California and Florida is far from a full-scale return to pre-exodus levels. It’s characterized by caution, precision, and a focus on rewarding mitigation.

Targeted Underwriting

Insurers are not simply opening the floodgates. Instead, they are:

- Segmenting High-Risk Areas: Within traditionally high-risk counties, they are identifying specific neighborhoods or even individual blocks that exhibit lower risk profiles due to geographic features, community-wide mitigation efforts (e.g., hardened infrastructure, better firebreaks), or individual homeowner actions.

- Incentivizing Mitigation: Homeowners who invest in fire-resistant roofing, clear defensible space, elevate their homes, or install hurricane-resistant windows are now more likely to qualify for coverage, and potentially at more favorable rates. Satellite data can verify these mitigation efforts, providing tangible proof.

- Dynamic Pricing: The ability to continuously monitor risk factors means pricing could become more dynamic, adjusting as environmental conditions change or as homeowners undertake new mitigation measures.

Partnership with Regulators and Communities

A sustainable re-entry also requires collaboration. Insurers are engaging more actively with state regulators to advocate for sensible building codes, investment in infrastructure hardening, and reforms to curb litigation abuses (especially in Florida). They are also working with local communities to support wildfire prevention programs and flood resilience initiatives. The data from satellite modeling provides a common ground for these discussions, offering objective, verifiable insights into risk.

Challenges Remain: Regulation and Litigation

Despite technological advancements, significant headwinds persist. In California, the “rate modernization” efforts are slow, and the approval process for premium increases remains cumbersome. In Florida, while some legislative reforms have aimed to curb litigation, the effects are still being fully realized. Insurers emphasize that technology alone cannot solve all market challenges; a stable and predictable regulatory and legal environment is equally crucial for long-term commitment.

5. How to “Pass” the Satellite Exam (2026 Guide)

If you live in Florida or California, your house is being scanned right now. Here is how to prepare your property for the “invisible inspection” and secure insurance:

California (Wildfires): Create “Defensible Space”: The satellite looks for vegetation density. Clear dry bushes within 5 feet of the house. Clean leaves from gutters (the satellite sees potential heat spots).

Florida (Hurricanes): The Roof is King: AI analyzes roof geometry and condition. If shingles are missing or discoloration (a sign of weakness) is visible from space, you will be flagged as “High Risk.” Repair any visible damage before applying for renewal.

Do Not Lie: In the past, you could say you didn’t have a pool or trampoline. Now, the satellite sees it. Ensure your declaration matches the visual reality of your yard.

6. Final Verdict: Big Brother to the Rescue?

Satellite technology has brought insurers back, which is a financial relief. But the price is constant surveillance. Your insurance premium now fluctuates in real-time based on whether you mow your lawn or clean your roof. The Question: Do you feel safer knowing you are evaluated individually, or does it worry you that insurers have an “eye in the sky” watching your property 24/7? Share your opinion below.