Projections Show Increase in U.S. Health Insurance Premiums for 2026

New York, NY — The American healthcare landscape is bracing for a significant financial shift as we enter 2026. According to the latest data from leading health policy analysts, actuarial firms, and federal regulators, projections show a sharp increase in U.S. health insurance premiums for 2026 across nearly all market segments.

While the last decade saw relatively moderate annual increases, the 2026 cycle is expected to be one of the most challenging in recent history. From the Individual Marketplace to employer-sponsored plans and Medicare Advantage, the “affordability crunch” is reaching a tipping point, driven by a complex intersection of drug costs, policy expirations, and persistent medical inflation.

1. The Magnitude of the 2026 Premium Surge

Data from the KFF (Kaiser Family Foundation) and various state-level insurance filings indicate that the individual market and small group sectors will face the steepest climbs.

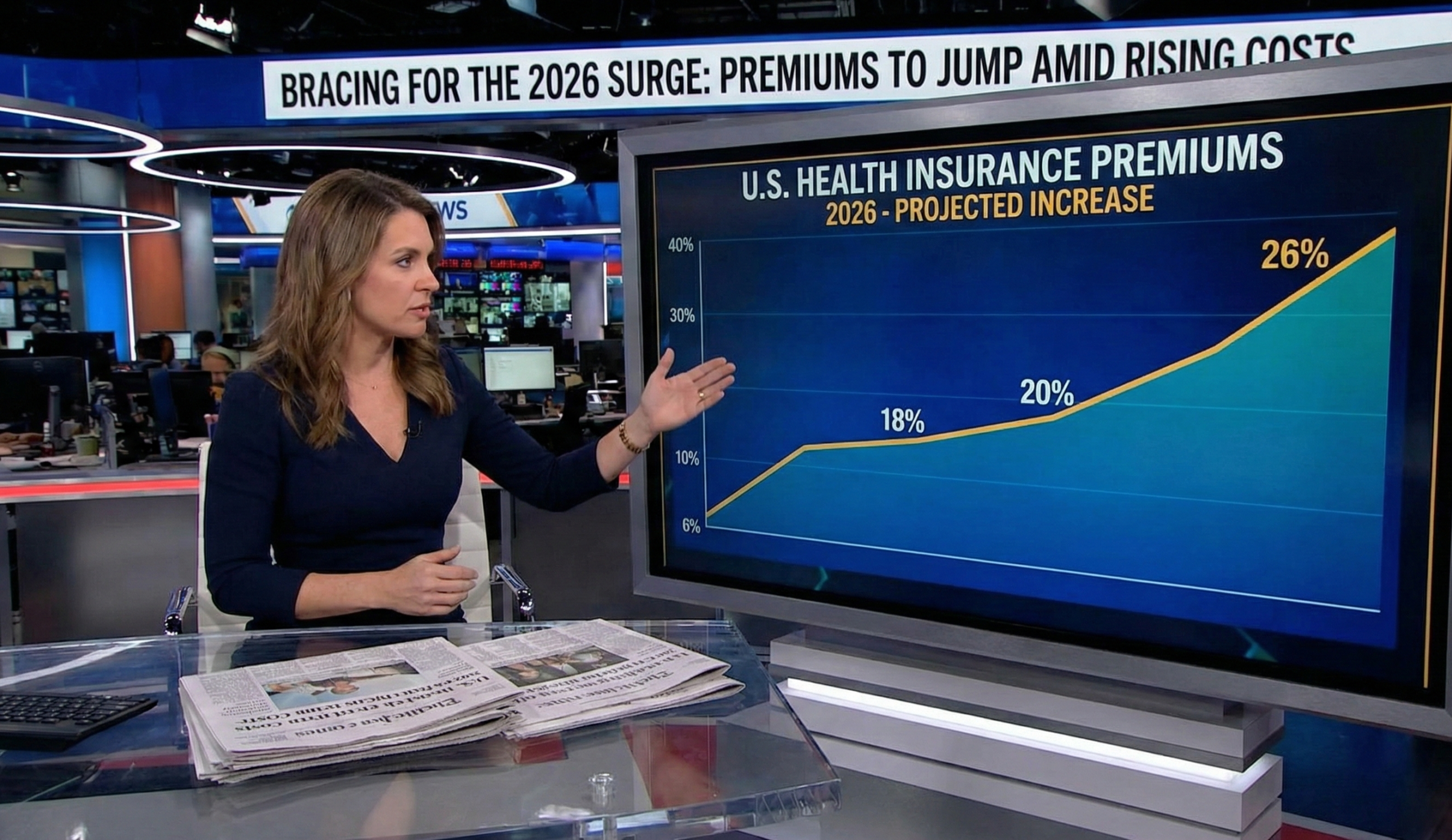

ACA Marketplace (Individual Market)

Marketplace insurers are proposing gross premium increases averaging between 18% and 26% for 2026. This represents the most significant rate change since 2018. In some states, insurers have requested hikes as high as 30% to 50%, citing a worsening risk pool and the potential expiration of federal assistance programs.

Employer-Sponsored Insurance

For the approximately 160 million Americans covered through their jobs, the news is equally sobering. Projections from Mercer and Aon suggest that the average total health benefit cost per employee will exceed $18,500 in 2026—a jump of nearly 7% to 9.5%. This marks the fourth consecutive year of elevated growth, far outpacing general wage increases and general inflation.

Medicare Advantage

In the public-private sector, the Centers for Medicare & Medicaid Services (CMS) finalized a 5.06% average reimbursement increase for Medicare Advantage plans in 2026. While this is an infusion of nearly $25 billion into the system, many insurers argue that it is insufficient to cover the rising utilization of services, leading many to predict higher out-of-pocket costs or reduced “extra” benefits for seniors in the coming year.

2. Deep Dive: The “Ozempic Tax” on Your Premium

Why is your insurance going up if you didn’t go to the doctor this year? Blame the “GLP-1 Effect.”

- The Cost: Drugs like Wegovy and Zepbound cost $1,000+ per month. As millions of Americans start taking them for weight loss, insurers are passing that massive bill to everyone in the risk pool.

- The Math: Actuaries estimate these drugs alone are adding 3% to 5% to your premium increase.

- The Result: We are moving from paying for “sick care” (surgeries) to paying for “lifestyle maintenance” (chronic weight management), and the system hasn’t figured out how to afford it yet.

3. Key Drivers: Why are Premiums Rising so Sharply?

The 2026 premium spike is not the result of a single factor but rather a “perfect storm” of economic and clinical drivers.

The “GLP-1 Effect”: Obesity and Diabetes Medications

Perhaps the most cited factor in 2026 filings is the explosive demand for GLP-1 receptor agonists such as Ozempic, Wegovy, and Zepbound. These medications, while highly effective for Type 2 diabetes and obesity, carry monthly list prices often exceeding $1,000. Two-thirds of large employers now report that GLP-1s have a “significant” impact on their pharmacy spend. Some actuaries estimate that these drugs alone are responsible for adding 3% to 5% to the overall premium trend in certain plans.

The Expiration of Enhanced Tax Credits

A critical policy deadline looms at the end of 2025. The enhanced premium tax credits—originally passed during the pandemic and extended through 2025—are set to expire unless Congress acts. If these subsidies disappear, KFF estimates that currently subsidized enrollees in the ACA Marketplace will see their monthly premium payments more than double, increasing by an average of 114%. Insurers are already pricing in the “morbidity risk” that healthier people will drop coverage if it becomes too expensive, leaving a sicker, more costly pool of enrollees.

Specialty Drugs and Gene Therapies

Beyond weight-loss drugs, the pipeline for specialty biologics and “one-and-done” gene therapies is expanding. Treatments for rare conditions, oncology, and autoimmune diseases now frequently cost upwards of $2 million per patient. For small to mid-sized employer groups, a single high-cost claimant can shift the entire plan’s financial trajectory.

Labor Shortages and Provider Consolidation

The healthcare sector continues to grapple with a persistent shortage of nurses and specialists. To retain staff, hospitals have had to increase wages, costs which are ultimately passed on to insurers through higher contract rates. Furthermore, the continued consolidation of hospital systems has reduced competition, giving large providers more leverage to demand higher reimbursement rates from insurance carriers.

4. Impact on Employers: A Search for Value

As health benefit costs approach nearly $20,000 per employee, businesses are being forced to rethink their strategy. For the readers of PolicyNewsHub.com, the following trends are defining the employer response in 2026:

- Shifting Costs to Workers: Approximately 60% of employers indicate they will make changes to plan design in 2026, often involving higher deductibles or larger employee contributions to monthly premiums.

- Narrow Networks and Centers of Excellence: To control costs, more companies are steering employees toward “High-Performance Networks” or specific hospitals that have proven better outcomes at lower costs for complex surgeries like joint replacements or cardiac care.

- The Rise of Level-Funding: Small and mid-sized businesses are increasingly abandoning traditional “fully-insured” models in favor of level-funded or captive insurance models, which allow them to retain some of the savings if their employees are healthier than expected.

5. Survival Guide: How to Beat the Rate Hike

Don’t just auto-renew. Use these 3 strategies during Open Enrollment to keep your costs down:

- Switch to “Silver” with Caution: If subsidies expire, “Silver” plans might become the most expensive due to “cost-sharing reduction” loading. Look at Bronze plans paired with an HSA (Health Savings Account) to lower your monthly fixed cost.

- Check the “Formulary” List: If you take expensive meds, check the 2026 drug list before buying. Many insurers are moving brand-name drugs to “Tier 4” (higher cost) to save money.

- Ask HR for a “Buy-Down”: If you have employer coverage, ask if they offer a High-Deductible Plan (HDHP) with an HSA match. It’s often mathematically cheaper than paying a high premium for a PPO you rarely use.

6. Final Verdict: Is the System Breaking?

We are facing the biggest premium spike in a decade. Families are being asked to pay nearly $20,000 a year for coverage they might not even use. The Big Question: Are you willing to pay higher premiums so that others can access weight-loss drugs? Or should insurers exclude lifestyle medications to keep costs down for everyone else? Tell us your opinion below.