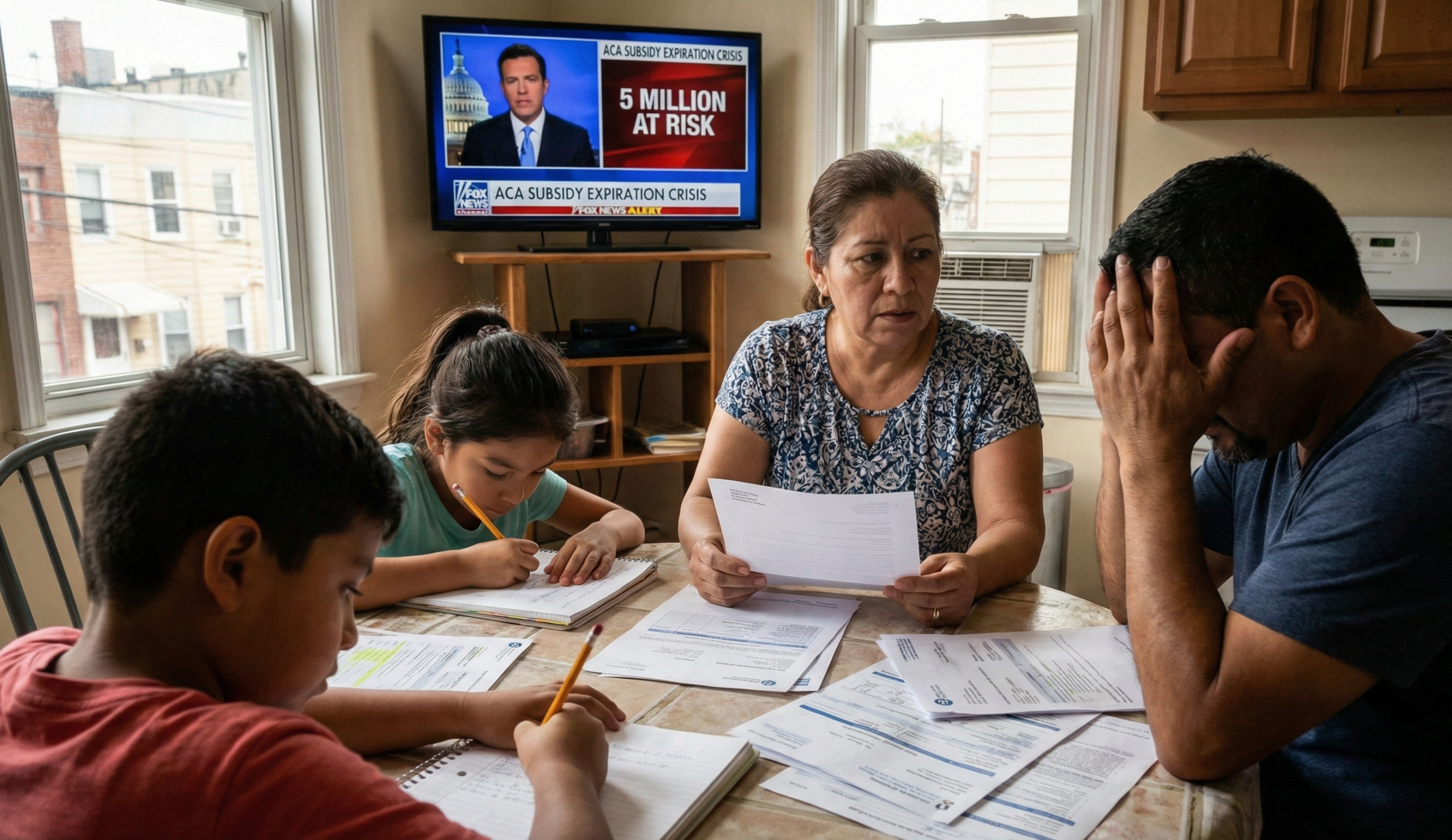

Nearly 5 Million Latinos Could Lose Health Insurance in the U.S. if Key Subsidies Disappear: A Growing Crisis for Equity and Access

WASHINGTON, D.C. — The landscape of healthcare in the United States is standing at a precarious crossroads. While the nation has reached record-low uninsured rates over the past few years, a looming legislative deadline threatens to dismantle these gains, with one community positioned at the epicenter of the fallout: the Latino population.

Recent projections from health policy analysts and non-partisan think tanks suggest that nearly 5 million Latinos are at risk of losing their health insurance coverage if the enhanced subsidies for the Affordable Care Act (ACA) Marketplace are allowed to expire. As we approach the 2026 fiscal cycle, the expiration of these federal financial supports—originally enacted under the American Rescue Plan Act (ARPA) and extended by the Inflation Reduction Act (IRA)—could trigger a reversal of decades of progress in closing the racial and ethnic coverage gap.

1. The Mechanism of the Crisis: Understanding Enhanced Subsidies

To understand why the Latino community is uniquely vulnerable, it is essential to examine the role of Advanced Premium Tax Credits (APTCs). The enhanced subsidies introduced in 2021 significantly increased the amount of financial assistance available to individuals purchasing insurance through the Marketplace.

The “Zero-Premium” Effect

The subsidies ensured that individuals with incomes between 100% and 150% of the federal poverty level could enroll in “Silver” plans with $0 monthly premiums. For many Latino families—who are disproportionately represented in low-to-mid-wage sectors such as hospitality, construction, and agriculture—this removed the single largest barrier to entry: upfront cost.

Elimination of the “Subsidy Cliff”

Before these enhancements, individuals earning more than 400% of the federal poverty level were ineligible for any tax credits. The current subsidies eliminated this “cliff,” capping premium costs at 8.5% of a household’s income. This shift allowed many “middle-class” Latino entrepreneurs and self-employed professionals to afford private insurance for the first time.

2. Deep Dive: Why the “Gig Economy” is Vulnerable

Why is the Latino community at the epicenter of this crisis? It comes down to Employment Structure.

- The Entrepreneur Gap: Latinos start small businesses at a faster rate than any other group. But being your own boss means no corporate HR department to pay for your insurance. You rely 100% on the Marketplace.

- The “Zero-Premium” Lifeline: The current subsidies allowed a freelance carpenter or a Uber driver to get top-tier insurance for nearly free.

- The Cliff: If this aid vanishes, these entrepreneurs aren’t just losing a discount; they are being priced out of the healthcare system entirely.

3. Why Latinos are the Most Impacted Demographic

The Latino community has historically faced the highest uninsured rates of any racial or ethnic group in the United States. While the ACA helped reduce these rates significantly, the community remains highly sensitive to price fluctuations in the insurance market.

Geographic Concentration in Non-Expansion States

A significant portion of the Latino population resides in states that have not expanded Medicaid, such as Texas and Florida. In these regions, the ACA Marketplace is often the only viable option for affordable coverage. Without the enhanced subsidies, premiums in these states are expected to skyrocket, forcing millions of families to choose between paying for healthcare or covering basic necessities like rent and groceries.

Workforce Dynamics

Latinos are more likely to work in small businesses or as independent contractors (gig economy workers) who do not have access to employer-sponsored insurance. Consequently, they rely more heavily on the individual Marketplace. Data shows that Latino enrollment in the Marketplace has surged by over 40% since the enhanced subsidies were introduced, indicating a direct correlation between affordability and participation.

4. The Economic Ripple Effect: Beyond Premiums

The loss of insurance for 5 million Latinos is not just a healthcare issue; it is a macroeconomic threat. When individuals lose coverage, the entire financial ecosystem of the U.S. healthcare system feels the strain.

Increased Uncompensated Care Costs

When the uninsured get sick, they often turn to Emergency Departments for care. This leads to a spike in uncompensated care costs for hospitals, particularly in rural and underserved urban areas. These costs are eventually passed down to the general public in the form of higher taxes and increased costs for private insurance.

Loss of Preventative Care

Latino communities already face higher rates of chronic conditions such as diabetes and hypertension. Coverage allows for consistent management of these diseases. If 5 million Latinos lose insurance, we will see a shift from preventative medicine to crisis medicine, resulting in poorer health outcomes and higher long-term costs for the federal government.

5. Projections for 2026: The Numbers Behind the Fear

As policy experts look toward the 2026 coverage year, the data is sobering. If the subsidies are not extended, it is estimated that:

- The average Latino family of four could see their monthly health insurance premiums increase by $200 to $400.

- In “high-cost” states, premiums could effectively double for those previously receiving the most assistance.

- Marketplace enrollment is projected to drop by nearly 25% among Hispanic enrollees, reversing nearly all the gains made in the last five years.

6. Family Action Plan: Preparing for 2026

Don’t wait for Congress to decide your fate. Take these steps during the next Open Enrollment:

Check Your Income Estimate: Subsidies are based on estimated annual income. If your income has dropped, update your Marketplace application immediately to maximize your tax credit.

Look for “Cost Sharing Reductions” (CSR): Only “Silver” plans offer CSRs (lower deductibles). Even if the premium goes up, a Silver plan might still be cheaper than a “Bronze” plan when you actually visit the doctor.

Consult a Navigator: Brokers are helpful, but non-profit “Health Navigators” specialize in finding subsidies for Latino families. Their services are free.

7. The Human Cost: A Community at Risk

Beyond the statistics are the stories of millions of individuals. For many Latino families, health insurance is the difference between financial stability and a single medical bill leading to bankruptcy. The community has made strides in health literacy and insurance enrollment, largely because the “enhanced” system made the value proposition clear: healthcare you can actually afford.

If the subsidies disappear, the “trust gap” between the government and the Latino community may widen. Many may view the system as unreliable, leading to a long-term disengagement from formal healthcare structures.

8. Final Verdict: A Step Backward for Equity?

For the last few years, the gap in uninsured rates between Latinos and the rest of the U.S. was finally closing. Now, we are on the verge of undoing a decade of progress. The Big Question: Should the government make these “temporary” subsidies permanent to protect public health, or is the cost to the taxpayer too high? Share your thoughts below.